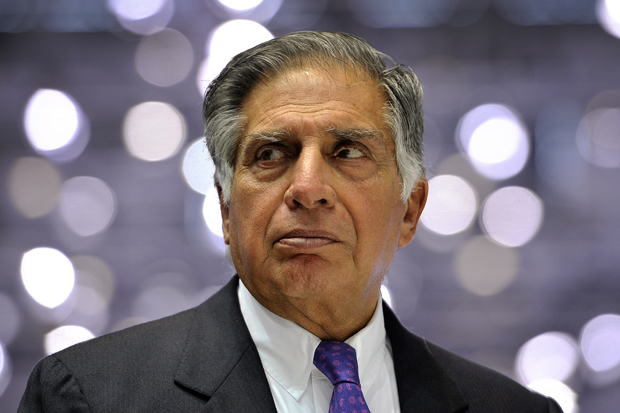

If asked to pick the UK’s inward investor of the century so far I would, without hesitation, name Ratan Tata, the anglophile former patriarch of the eponymous Indian conglomerate that bought Tetley the tea-maker for £271 million in 2000, Corus the Anglo-Dutch steel-maker for £6.2 billion in 2007, and Jaguar Land Rover — from Ford — for £1.3

Already a subscriber? Log in

Get 10 issues

for $10

Subscribe to The Spectator Australia today for the next 10 magazine issues, plus full online access, for just $10.

- Delivery of the weekly magazine

- Unlimited access to spectator.com.au and app

- Spectator podcasts and newsletters

- Full access to spectator.co.uk

Or

Unlock this article

You might disagree with half of it, but you’ll enjoy reading all of it. Try your first month for free, then just $2 a week for the remainder of your first year.

Comments

Don't miss out

Join the conversation with other Spectator Australia readers. Subscribe to leave a comment.

SUBSCRIBEAlready a subscriber? Log in