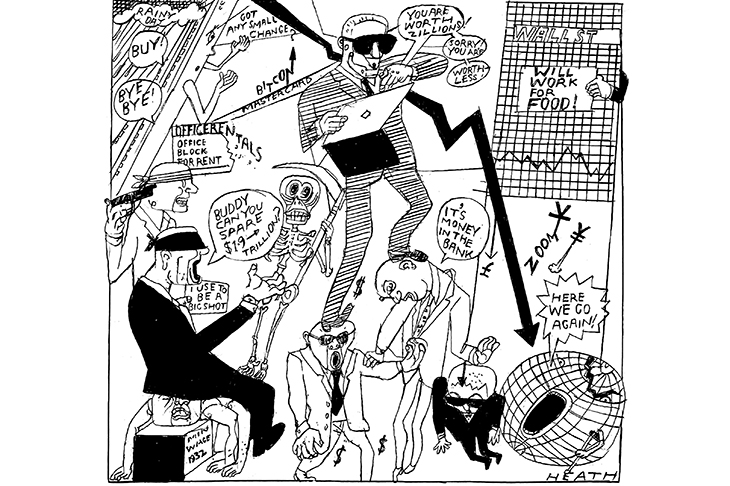

Shops are boarded up. More than four million people are on furlough with little idea of whether they will have jobs to go back to. Global trade has hit levels last seen a decade ago, and government deficits are soaring, while most developed economies have seen output shrink by 10 per cent, a collapse not seen since the Great Depression of the 1930s.

Already a subscriber? Log in

Get 10 issues

for $10

Subscribe to The Spectator Australia today for the next 10 magazine issues, plus full online access, for just $10.

- Delivery of the weekly magazine

- Unlimited access to spectator.com.au and app

- Spectator podcasts and newsletters

- Full access to spectator.co.uk

Or

Unlock this article

You might disagree with half of it, but you’ll enjoy reading all of it. Try your first month for free, then just $2 a week for the remainder of your first year.

Comments

Don't miss out

Join the conversation with other Spectator Australia readers. Subscribe to leave a comment.

SUBSCRIBEAlready a subscriber? Log in