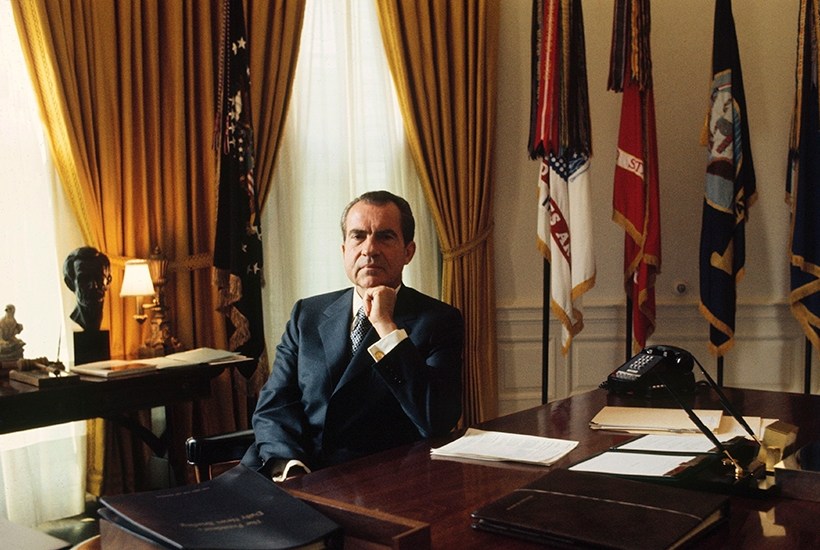

The dotcom bubble. The financial crisis of 2008 and 2009. The oil price spiral of the 1970s. The launch of the single currency. It would be fun, in a nerdish kind of a way, to debate which was the most seismic economic event of postwar history. But in fact the answer would be this: the ‘Nixon shock’, a fateful day when the final link between gold and the money you carry around in your pocket, or on your bank card, was finally severed.

Already a subscriber? Log in

Get 10 issues

for $10

Subscribe to The Spectator Australia today for the next 10 magazine issues, plus full online access, for just $10.

- Delivery of the weekly magazine

- Unlimited access to spectator.com.au and app

- Spectator podcasts and newsletters

- Full access to spectator.co.uk

Or

Unlock this article

You might disagree with half of it, but you’ll enjoy reading all of it. Try your first month for free, then just $2 a week for the remainder of your first year.

Comments

Don't miss out

Join the conversation with other Spectator Australia readers. Subscribe to leave a comment.

SUBSCRIBEAlready a subscriber? Log in