When George Osborne visited Sweden, Finland and Denmark the stock markets of each country promptly fell by about 5 per cent. As soon as he left, they recovered. A coincidence, of course: Osborne’s tour coincided with stock-market jitters, but this nonetheless forced him to look over the precipice — and panic. Britain, he warned, was ‘not immune to what goes on in the world’. Not for the first time, we saw his lips moving but heard Gordon Brown’s voice. ‘We are much better prepared than we would have been a few years ago for this kind of shock,’ he added.

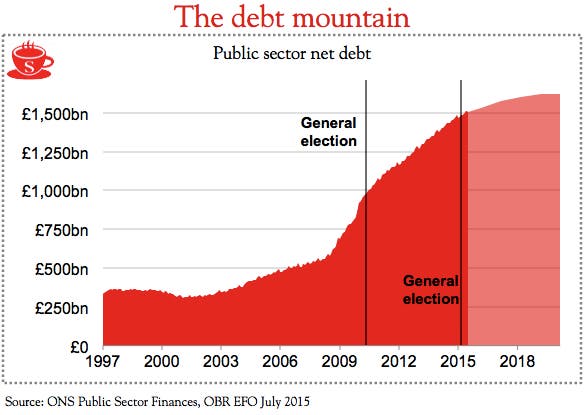

If only this were true. As the Chancellor knows, we are far more vulnerable than we were last time. In 2008, the national debt was 37 per cent of GDP — a fairly low level, inherited from the Tories, that allowed Labour to borrow its way out of the crisis. Now, the national debt stands at 80 per cent of GDP and we have no more room for manoeuvre. While lecturing everyone about austerity, Osborne has swollen the national debt to some £1.5 trillion and has not finished yet.

This is not QE-style imaginary money but real debt that has to be repaid by real British taxpayers, working out at about £56,000 per household.

To be sure, Osborne inherited public finances that were out of control — but he has been in no rush to correct things. At first, he said he’d balance the books in five years’ time. He has now given himself ten years because of a freakish blip in world markets. Interest rates everywhere were coming crashing down, so for all of his hair-shirt rhetoric, he could keep running up debt and get away with it.

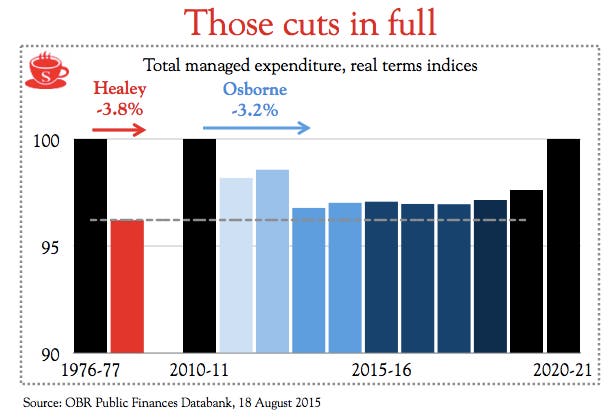

So far, he has been right. It has suited Labour to accuse him of harsh cuts, despite the fact that he has shaved just 2.9 per cent off state spending in five years.

Like a drunk holding 2 a.m. toasts to the notion of sobriety, the Chancellor salutes the notion of fiscal prudence while borrowing £190 million a day. He offers words of advice for politicians in Athens, while running up a deficit six times larger than that of Greece. This week, he said that the financial crisis was a reminder for all governments to put their financial houses in order — yet no one needs this advice more than him. The British government is still the worst debt addict in the continent.

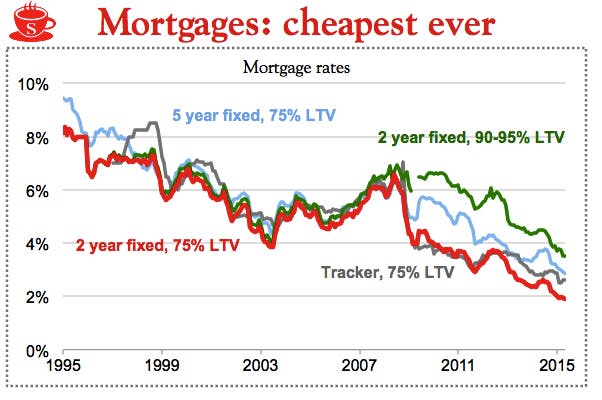

As Martin Vander Weyer argues, the stock market crash looks as if it is a test, rather than the real thing. It’s hard to argue that shares are overpriced, as they were at the peak of the last bull market; valuations are around the historical average. The glaring anomaly is the absurdly low cost of borrowing. British banks have spent much of the past few years lending money at rates below inflation: in effect, paying people to borrow. This is just as alarming as the old days of 110 per cent mortgages. Crazy low interest rates mean crazy high house prices, as many would-be house buyers will agree. Yes, there is a lack of houses, but prices are being pushed higher by absurdly cheap lending.

There are not many certainties in politics or economics, but one thing is for sure: we will have a future financial crisis. And how prepared is Britain? The look of panic on Osborne’s face during interviews last week gave this away. He has bet the house (and other people’s houses) on there being no new crash, having become addicted to this new level of cheap debt. The average two-year mortgage fix is 1.9 per cent.

If this were to double, it would still be less than half the rate it was before the last crash, yet would risk pushing many households towards bankruptcy. And if his government were to be charged normal rates of interest on its debts, it would trigger a far deeper fiscal crisis.

The Chancellor may still prove lucky. There has been much talk about when the Bank of England will raise its rates, but not much discussion about the fact that the markets do not expect a return to the normal rates of 5 per cent. Instead, they predict a crawl back to about 2 per cent.

Long-term forecasts show an era of zero real interest rates lasting for about 20 years. Lots of decisions are being made on this basis, including those of HM Treasury. So the financial markets imagine that we’re entering a debtor’s paradise — which will be hell for Britain’s savers.

In 2007, the same market forecasters assured us that we had a ‘Goldilocks economy’ — not too hot, not too cold. There was talk of a ‘great moderation’ and an end to the era of crashes. How dangerously naive that all sounds now. The Chancellor may still be young, but he has lived through enough turbulence to know that none of these forecasters can be relied upon. They assure us that this week has been about nerves, not about a new bubble or a wider correction. The Chancellor will have to hope that they are right.

Got something to add? Join the discussion and comment below.

Get 10 issues for just $10

Subscribe to The Spectator Australia today for the next 10 magazine issues, plus full online access, for just $10.

Comments

Don't miss out

Join the conversation with other Spectator Australia readers. Subscribe to leave a comment.

SUBSCRIBEAlready a subscriber? Log in