Government borrowings are skyrocketing as you read this. Unfashionable though it is to worry about this, there are still some of us who do.

Among the propositions made to dismiss these concerns is that Australia’s government debt is much lower than that of other advanced countries, so why worry? Following this logic, there is scope to borrow much more than already planned.

As a matter of arithmetic, it is undoubtedly true that Australia has a much smaller public debt burden than the average of advanced countries; but how meaningful is this? As a justification or excuse for running up more debt, it is wearing thin.

We cannot explain away our own fiscal vulnerability by pointing to the greater vulnerability of others. Comparisons with the rest of the world should not ignore the absolute levels. It was one thing to draw comfort when our debt was low or even negative (in net terms) as it was before the GFC. But such comparisons carry much less weight when we are heading for net debt of more than 50% of GDP.

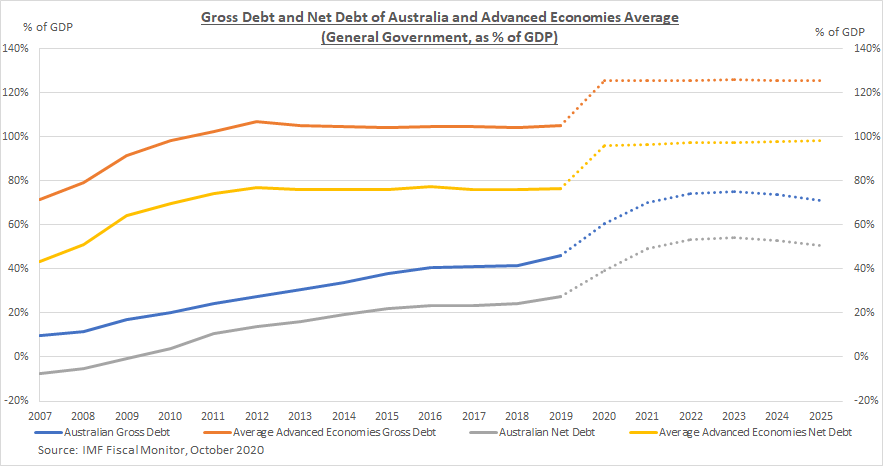

The chart below, based on IMF compilations of general government gross and net debt of its member countries, shows what has been happening and what is projected to happen in Australia and advanced countries on average.

Debt has risen in two episodes since 2007: in the GFC of 2008-09 and in the coronavirus pandemic. For example, net debt of advanced economies rose from an average of 43% of GDP in 2007 to 77% in 2012, remained around that level until 2019, and this year is estimated to rise from 77% to 96%.

Debt has risen in two episodes since 2007: in the GFC of 2008-09 and in the coronavirus pandemic. For example, net debt of advanced economies rose from an average of 43% of GDP in 2007 to 77% in 2012, remained around that level until 2019, and this year is estimated to rise from 77% to 96%.

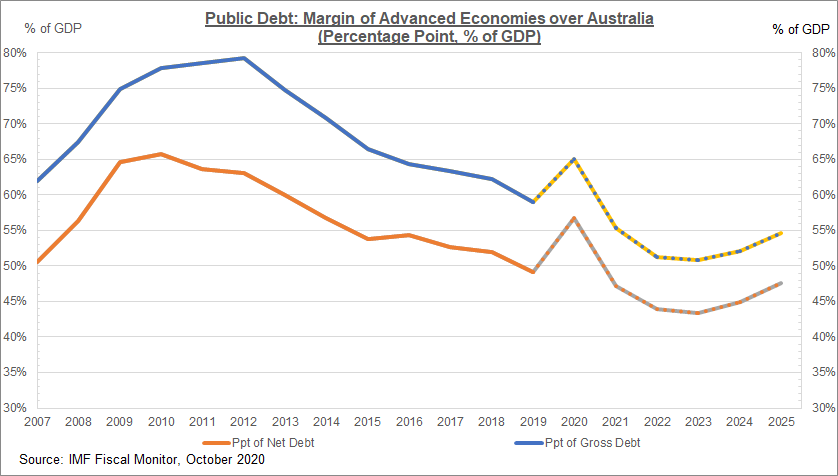

Australia was less affected by the GFC and the increase in debt in the five years from 2007 lagged other advanced countries. However, we then made up for that lag in the next seven years — so by 2019, our net debt had risen as much, compared with 2007, as the advanced country average. This is shown in the second chart, which demonstrates how the margin of average advanced country debt over Australia’s debt initially widened but by 2019 had fallen back to what it was in 2007.

There are several reasons why Australia’s relative position is not as reassuring as often claimed:

There are several reasons why Australia’s relative position is not as reassuring as often claimed:

- The margin of advantage, having peaked in 2012, is projected to shrink up to 2023.

- That shrinking advantage is measured against a level of debt in other countries that is itself rising dramatically. The proposition that we are better off than an international benchmark wears thin when the benchmark itself is shifting and we are shifting with it.

- This means that Australia will soon have levels of gross and net debt equivalent to the averages of advanced countries about 12 years ago.

- The advanced country average conceals huge variation among its constituent members. In fact, it is Japan, the US, the UK and a handful of EU countries that account for the average being so high, and compared with other countries Australia’s debt is similar or higher.

- It is a mistake to think that the other countries with higher debt levels than Australia have not been harmed and that this therefore shows that debt is benign. There are persuasive arguments that high public debt levels have slowed economic growth in several countries since the GFC.

- Moreover, it should not be assumed that Australia, as a capital importing country that needs to remain attractive as a destination for investment, has the same ability to carry public debt as other countries.

- It is not only public debt that matters to assessments of financial vulnerability. While Australia has lower public debt than some other advanced countries, we have extremely high household debt and substantial corporate debt.

International comparisons are just one aspect of a much wider debate on public debt. There are many reasons to be concerned about the permissive attitude to debt now apparent in economic policy circles.

Robert Carling is a Senior Fellow at the Centre for Independent Studies.

Got something to add? Join the discussion and comment below.

Get 10 issues for just $10

Subscribe to The Spectator Australia today for the next 10 magazine issues, plus full online access, for just $10.

Comments

Don't miss out

Join the conversation with other Spectator Australia readers. Subscribe to leave a comment.

SUBSCRIBEAlready a subscriber? Log in