Over many years now, superannuation funds have been orientating their investments towards options that avoid unapproved Environmental and Social goods or Governance structures (ESG).

The governance part involves avoiding firms with boards and senior executives containing too many white males and, therefore, inadequate ‘diversity’. The Environmental and Social parts used to mean avoiding firms in the defence and tobacco industries, but the pariahs in the modern woke world are hydrocarbons – coal, gas, and oil. These and some other industries, like forestry and nuclear power, are targeted by the legions of non-government organisations which are largely funded by governments and wealthy elites, some of whom owe their fortunes to the industries they now vilify.

Superannuation and retirement funds follow in the wake of this activism. The reasons for this vary. In many cases in Australia it is due to the funds being dominated by trade union representatives – people who ideologically oppose what they see as an ‘unacceptable face of capitalism’ to which they are inherently suspicious.

Funds in general – including those like BlackRock which vigorously embrace capitalism – have moved from passive investors, motivated by firms’ perceived future values, to active investors counselling company management to mend its ways and subscribe to the current fads. These include gender and race issues and, above all, anything perceived as contributing to the fabled global warming.

Productive businesses take such advice seriously since a major investor selling a firm’s shares depresses its value. In the process, this may also be lowering its ability to attract funds and even make it vulnerable to corporate raiders.

Hence Whitehaven, one of the few pure coal plays among listed Australian shares, has introduced a ‘Sustainability Report’ in which it, ‘recognises and supports the long-term goal of the Paris Agreement to limit global average temperature increases to below two degrees Celsius compared to pre-industrial levels’. Whitehaven is also exploring ‘carbon abatement opportunities for its Scope 1 and 2 greenhouse gas emissions, including options to generate and purchase carbon offsets’.

It is seldom that sentiment will prevail over genuine returns on investment. For most of us, most of the time, cupidity trumps a general disposition to sacrifice income and this has been the driving force of income growth that capitalism has delivered.

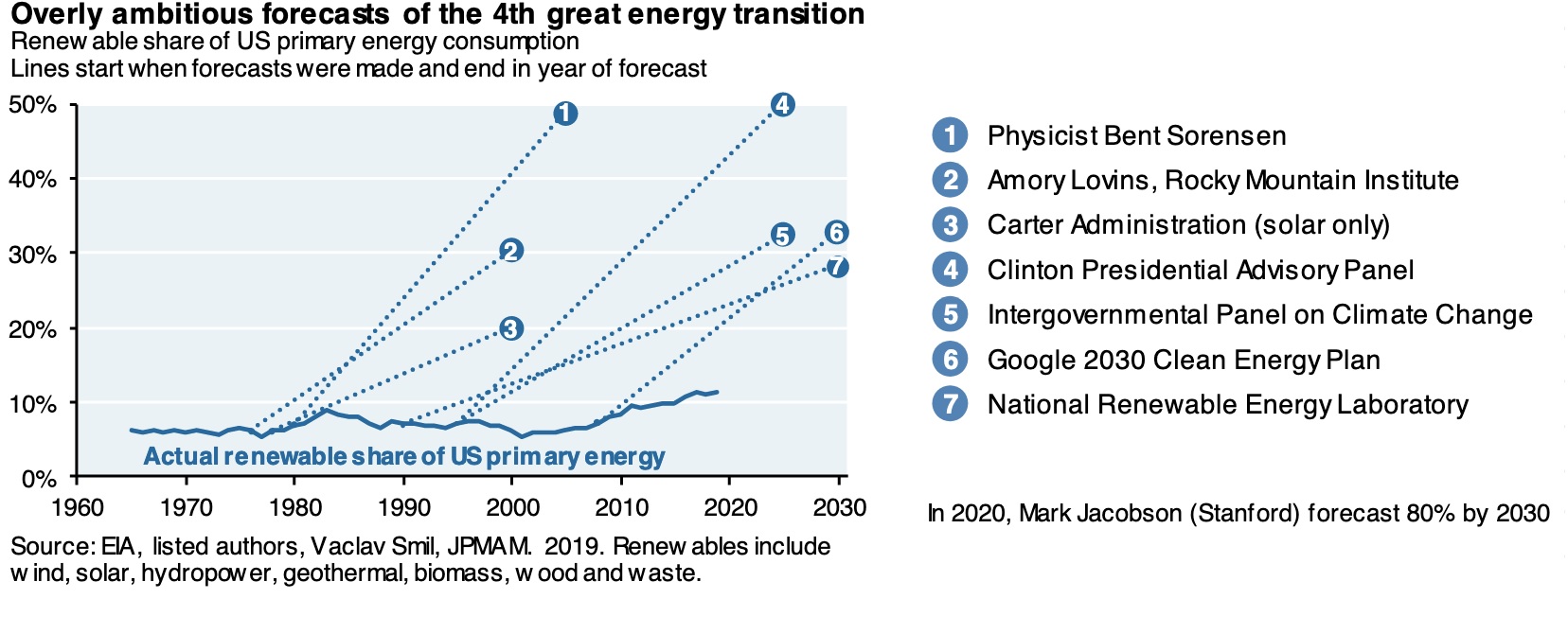

An early concern about the hype over green energy and the vilification of more traditional sources was registered by JP Morgan over six months ago. The advisory firm is as woke as any other, but observed the persistent over-promises of the ‘energy transition’ as illustrated in this diagram.

On this and other evidence, JP Morgan sorrowfully reflected that the world might fail to take up renewables as fast as they had hoped.

Recent developments have tended to confirm that those touting the impending death of hydrocarbons are, at the very least, somewhat premature. There has been a resurgence in interest in hydrocarbon businesses by investors who have noted their depressed share prices in the context of a growing realisation that their alternatives – wind and solar (together with the laughable claims for hydrogen) – cannot cut the mustard. The UK Daily Telegraph has reported, ‘Private equity firms spent £11.9b on European oil and gas businesses in 2021, compared to just £232m in 2020.’ The flip side of this has been the collapse of wind/solar energy plays. A package of global clean energy shares, including Iberdrola, Vestas, and Orsted, has fallen 45pc since a record peak a year ago.

Chant West monitors the performance of a wide variety of fund managers and publishes comparisons of selected range of Australian ‘growth funds’. A majority of these funds subscribe to ESG principles, especially avoiding coal, in assembling their investment portfolios. Such funds comprised nine out of the top ten performers in returns measured over the past ten years. To a major degree this has been due to the anti-hydrocarbon funds being overweight in tech shares, which have (until this month), performed well above the rest of the market. Those funds may also have benefited from a herd effect, whereby funds avoiding coal, gas, and oil firms have depressed their price while causing a bubble in favoured ‘ethical’ stocks.

In any event, in the latest year, although the top two performing funds avoid coal oil and oil, six of the ten do not.

| 2021 return | Hydrocarbon investments | |

| 1.Hostplus – Balance. | 19.1 | Avoid |

| 2. Sunsuper – Balanced | 16.5 | Avoid |

| 3. Christian Super My Ethical | 16 | No policy |

| 4. Mine Super Growth | 15.9 | No policy |

| 5. Telstra Super Balanced | 15.9 | No policy |

| 6. Suncorp Multi Manager Growth | 15.2 | No policy |

| 7. MLSC Horizon 4 | 15.1 | No policy |

| 8. AustralianSuper – Balanced | 15 | Exclude |

| 9. Plum Pre-mixed balanced | 15 | No policy |

| 10. Legal My Super Balanced | 14.8 | No policy |

Historically, the iron laws of markets saw stocks and shares being valued on expected performance unalloyed by sentiment. Recent years have seen this change as fund managers exited traditional energy shares but the reality may be in the process of being restored.