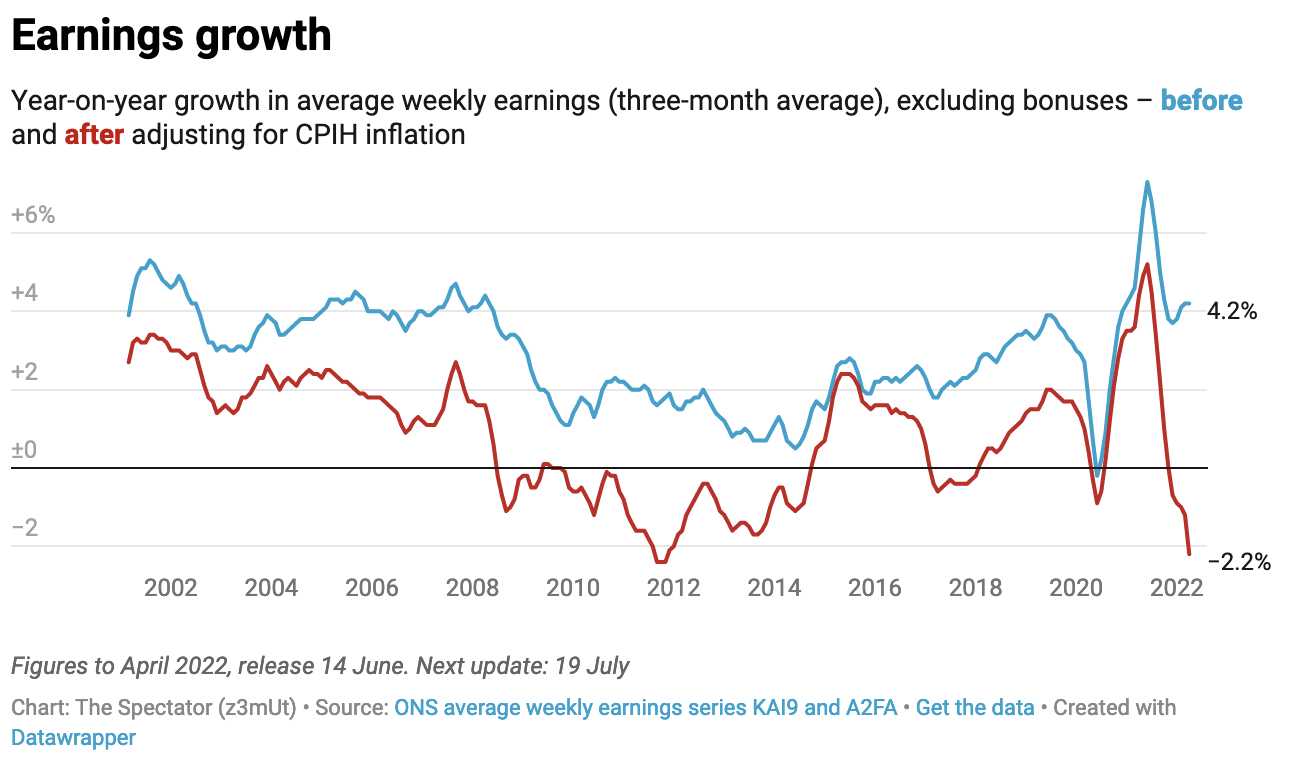

First the good news: the Office for National Statistics figures released today show that pay is rising at its fastest rate in two decades, with regular pay up by 4.2 per cent in the three months for February to April compared with a year earlier. Now the bad news: such is inflation that, in real terms, regular pay was actually down 2.2 per cent – lower than at any time in the past two decades except for a brief period in the autumn of 2011. So, yes, it isn’t just an illusion: we really are getting poorer. That is a big problem not just for households trying to make ends meet but also for the government, which at some point over the next two years will have to try to persuade voters to trust it with the economy.

If, to use the phrase of football managers, you wanted to take some positives out of this morning’s release they are these. Firstly, the last time that regular pay fell so sharply in real terms, it wasn’t followed by a recession. In fact, regular pay in real terms fell continuously between 2009 and the end of 2014 and still the economy managed to grow – so no one should take today’s figures as a sign that recession is inevitable (although plenty of other data might lead you to this conclusion).

Secondly, today’s figures suggest that high inflation is not leading to a wages-prices spiral. However hard they are trying or not trying, workers as a whole are not succeeding in pushing up wages to match inflation. The danger with inflation is that it becomes a feedback loop, with higher prices leading to higher wage demands, which in turn forces producers to recover their wage costs by pushing up prices and so on. If that is not happening we ought to expect inflation to fall as global supply chain issues are fixed.

However, there are very big political dangers hidden in today’s figures. If the government has anything which could be called a big idea it is ‘levelling up’ – the idea that income and wealth should rise fastest at the lower end of the scale so as to reduce the divisions between rich and poor. Today’s figures suggest that the opposite is happening. While regular pay fell in real terms, total pay (including bonuses) just about held its own against inflation, rising by 0.4 per cent over the 12 months to the period February-April. This was largely due to the finance and business sector, much of which is focused in the south east, where total pay rose by 10.6 per cent.

Thus the current situation with the economy can be summed up as follows: we are all getting poorer except for financiers, who have had a thumping good year. That is not the message you want to send out to voters in Wakefield or Devon ahead of next week’s by-elections.

The other danger for the government lies in public sector pay, which rose by only 1.5 per cent over the same period – a real-terms fall of nearly 5 per cent. That doesn’t necessarily mean that public sector workers are getting the worst deal just at the moment – many can look forward to index-linked pensions based on their final salary or lifetime earnings. Meanwhile, many private sector workers can only watch as their pension pots are struck by a decline in the value of shares and bonds. But that is probably not how public sector workers are going to see it. We already have strikes on the railways – we could be in for a very long summer and autumn of pay disputes as public sector workers try to protect their pay against inflation.

Got something to add? Join the discussion and comment below.

Get 10 issues for just $10

Subscribe to The Spectator Australia today for the next 10 magazine issues, plus full online access, for just $10.

Comments

Don't miss out

Join the conversation with other Spectator Australia readers. Subscribe to leave a comment.

SUBSCRIBEAlready a subscriber? Log in