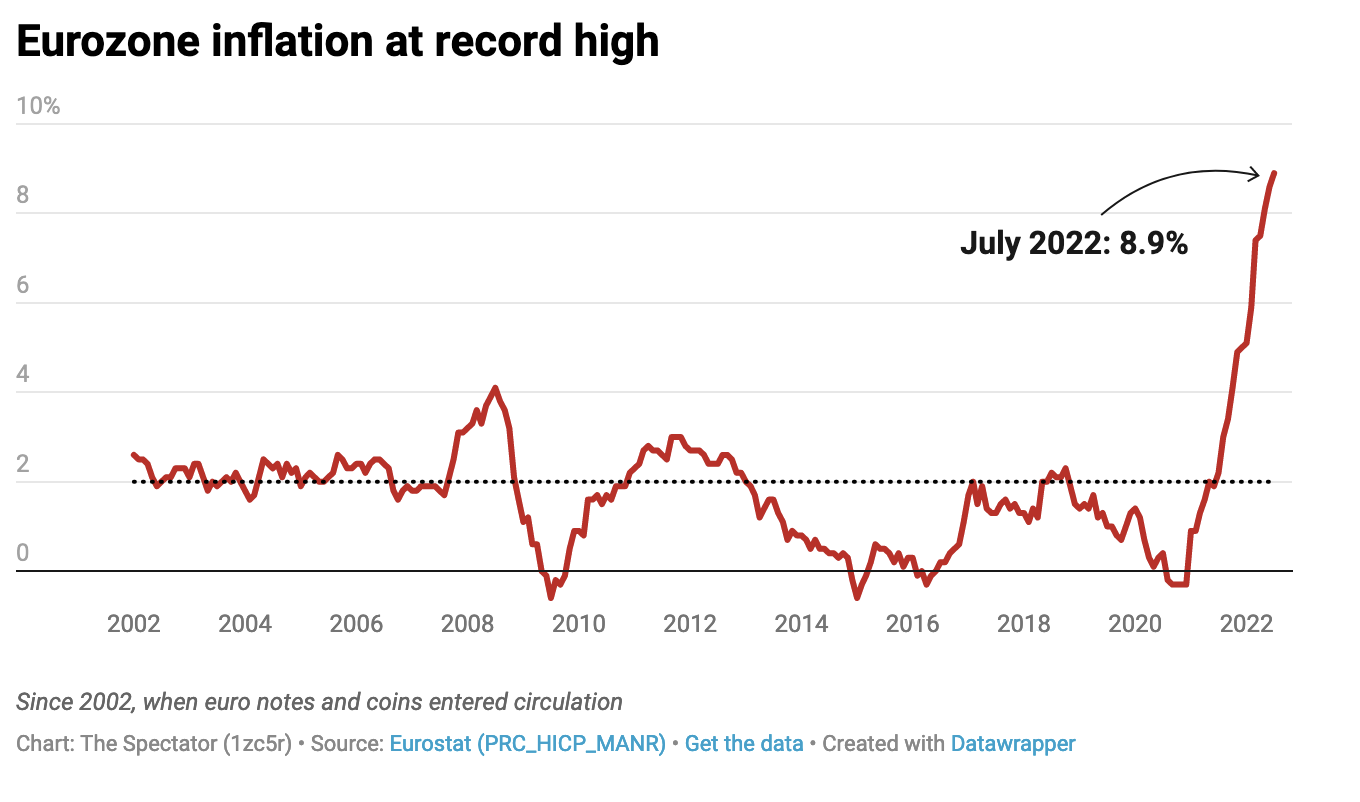

Is the eurozone heading for another 2010-style sovereign debt crisis? Today comes the news that inflation in the eurozone hit 8.9 per cent in the year to July. Although it is a record high, it is not as quite as towering as inflation in Britain – at 9.4 per cent. However, what it does do is expose the vulnerability of the eurozone – and how Italian public debt threatens to undermine it. This week, the yield on Italian ten-year government bonds rose to 3.5 per cent as investors began to wonder again if the country can honour its debts. Granted, it’s not quite as high at the rates of over 6 per cent which investors were demanding in 2012 – but it’s a sharp rise in recent times. There is another tranche of Italian public debt that is index-linked – around 10 per cent of its total debt – and which will now cost the Italy far more to service.

Italy is not the only country groaning under the burden of extra borrowing during the pandemic: Britain, too, is facing huge debt-servicing costs as a result of high borrowing and soaring inflation. Last month alone, the government paid an astonishing £19.4 billion on debt interest – twice what it paid the same time last year. To put this into context, the National Insurance rate hike was supposed to raise £12 billion a year.

But there’s a world of difference between Britain and the eurozone. In extremis, the Bank of England could always print the money required to repay investors in government debt (indeed, as it was effectively doing through quantitative easing). It would never be necessary for Britain to suffer the ignominy of defaulting on its debts. But a country – such as Italy – which doesn’t control of its own currency doesn’t have this option. If Italy cannot afford its debt repayments, its only option is to go to the European Central Bank and beg for help. Nor can Italy set its own interest rates to suit economic circumstances – it must live with an interest rate set by the ECB to cover the entire eurozone, made up of very different economies.

That’s what makes the eurozone so unstable. Current matters may not be as desperate as they were 12 years ago when Greece, Italy, Spain and others had to be bailed out. But still, they are heading in the wrong direction. ECB monetary policy won’t bring eurozone inflation under control: this month it raised its interest rate to 0 per cent from 0.5 per cent, the first rise since 2011. The eurozone is way behind the curve when it comes to fighting inflation – and may well suffer for that. That failure to act may see the eurozone become this year’s big financial story.

Got something to add? Join the discussion and comment below.

Get 10 issues for just $10

Subscribe to The Spectator Australia today for the next 10 magazine issues, plus full online access, for just $10.

Comments

Don't miss out

Join the conversation with other Spectator Australia readers. Subscribe to leave a comment.

SUBSCRIBEAlready a subscriber? Log in